Home Affordability

Everyone is ready to buy a home at different times in their lives. Understanding how affordability works and the main market factors that impact it may help those who are ready to buy a home narrow down their optimal window of time to make a purchase.

There are three main factors that go into determining how affordable homes are for buyers:

- Mortgage Rates

- Mortgage Payments as a Percentage of Income

- Home Prices

The National Association of Realtors (NAR), produces a Housing Affordability Index, which takes these three factors into account and determines an overall affordability score for housing. According to NAR, the index:

“…measures whether or not a typical family earns enough income to qualify for a mortgage loan on a typical home at the national and regional levels based on the most recent price and income data.”

Their methodology states:

“To interpret the indices, a value of 100 means that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home. An index above 100 signifies that family earning the median income has more than enough income to qualify for a mortgage loan on a median-priced home, assuming a 20 percent down payment.”

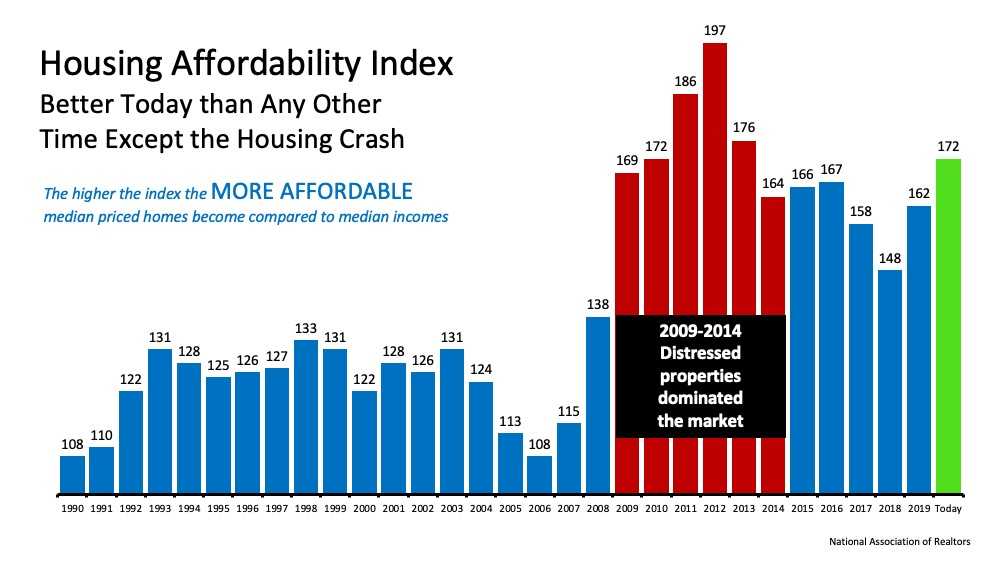

So, the higher the index, the more affordable it is to purchase a home. Here’s a graph of the index going back to 1990:

The green bar represents today’s affordability. We can see that homes are more affordable now than they have been at any point since the housing crash when distressed properties (foreclosures and short sales) dominated the market. Those properties were sold at large discounts not seen before in the housing market.

Why are homes so affordable today?

Although there are three factors that drive the overall equation, the one that’s playing the largest part in today’s homebuying affordability is historically low mortgage rates. Based on this primary factor, we can see that it is more affordable to buy a home today than at any time in the last seven years.

If you’re considering purchasing your first home or moving up to the one you’ve always hoped for, it’s important to understand how affordability plays into the overall cost of your home. With that in mind, buying while mortgage rates are as low as they are now may save you quite a bit of money over the life of your home loan.

Low Prices + Low Mortgage Rates = High Affordability

Prices have since recovered and mortgage rates have increased as the economy has gained strength. This has and will continue to impact housing affordability moving forward.

What You Need To Know About Down Payments

Saving for a down payment is sometimes viewed as one of the biggest obstacles for homebuyers, but that doesn’t have to be the case. As Freddie Mac says:

“The most damaging down payment myth—since it stops the homebuying process before it can start—is the belief that 20% is necessary.”

According to the most recent Home Buyers and Sellers Generational Trends Report from the National Association of Realtors (NAR), the median down payment for homes purchased between July 2019 and June 2020 was only 12%. That number is even lower when we control for age – for buyers in the 22 to 30 age range, the median down payment was only 6%.

You May Be Able To Afford More Home Than You Think

Working remotely, exercising, and generally spending more time than ever in our homes has changed what many people are looking for in their living space. However, some young homebuyers don’t feel they can afford a home that suits their growing needs and have decided to continue renting instead. That means they’ll miss out on some of the long-term benefits of owning a home. As an article recently published by NAR points out:

“Many young adults are underestimating how much they need for homeownership, the survey finds. Millennials underestimated how much home they can afford right now, how much interest they would pay over a 30-year mortgage, and how much home values appreciate, on average, over 10 years…”

Knowing how much home you can afford when starting the buying process is critical and could be the game-changer that gets you from renting to buying.

Homeownership Will Become Less Affordable the Longer You Wait

Finally, with mortgage rates starting to rise along with home prices appreciating, putting off buying a home now could cost you much more later. Sam Khater, Chief Economist at Freddie Mac, notes:

“As the economy progresses and inflation remains elevated, we expect that rates will continually rise in the second half of the year.”

Most experts forecast interest rates will rise in the months ahead, and even the smallest increase can influence your buying power. If you’ve been on the fence about buying a home, there’s no time like the present.

There’s No Place Like Home

If you feel ready to buy, purchasing a home this season may save you significantly over time based on historic affordability trends. Contact Oz Lending to speak to one of our loan specialists to determine if now is the right time for you to make your move.